China Takes the Lead in Organic Chemistry: A New Landscape for European Sourcing

China’s chemical industry is changing the rules of the game — European buyers can no longer ignore it

Published by Luigi Bidoia. .

Organic Chemicals Price Drivers

One of the most significant achievements of China's industry over the past decade—still largely overlooked by Western media—is the remarkable growth of its chemical sector. This success was officially recognized in 2024, when China became the world’s leading exporter of chemical products, surpassing not only the United States and Germany, but the entire European Union.

At the same time, another underreported development is the recent crisis of the German chemical industry: between 2021 and 2023, Germany’s chemical exports by volume dropped by 19%, while Dutch and Belgian exports declined less sharply. Notably, during the same period, exports from the German automotive sector—often described as the “sick man” of German industry—increased by 6%, underscoring the dramatic nature of the chemical sector's decline.

The crisis in the German chemical industry, combined with the challenges facing the chemical sectors in Belgium and the Netherlands, has important implications for European manufacturing SMEs. The erosion of a historically competitive advantage—affordable access to European basic chemicals—weakens their supply chain resilience and cost efficiency.

This article focuses in particular on basic organic chemistry, where Chinese industry has recently overtaken its European counterpart. In basic inorganic chemistry, this overtaking occurred over a decade ago and is now widely acknowledged as consolidated.

Leading Exporters in Basic Organic Chemistry

The two charts below show the leading exporters of basic organic chemical products in 2019—before the pandemic and the European gas crisis—and in 2024. An analysis of the data clearly shows the leap forward of China, which has distanced not only European countries but also the United States, currently the world's second largest exporter.

Among European countries, the Netherlands stands out, having moved from fifth to third place, overtaking Belgium. Within Europe, Switzerland shows remarkable progress: absent from the global top ten in 2019, it climbs to seventh place in 2024.

Among Asian countries, South Korea holds steady in seventh position, while Japan drops out of the global top ten.

It is reasonable to assume that one of the key factors behind the difficulties faced by Europe’s organic chemical industry—especially in Belgium and Germany—lies in the new gas price landscape. Alongside virgin naphtha, natural gas is a primary feedstock for the organic chemical industry. Due to the 2021–2022 energy crisis and the sharp drop in EU pipeline imports from Russia, gas prices in Europe have undergone a structural shift: whereas they ranged between €5 and €25/MWh in the decade before the crisis, over the past 24 months they have fluctuated between €26 and €52/MWh. Futures markets do not foresee prices falling below €30 in the next three years, reflecting financial market expectations that a return to pre-crisis levels is unlikely.

However, the gas price increase is not the only factor at play—otherwise, Switzerland’s strong performance over the past decade would be hard to explain. Still, higher gas prices have undeniably driven up relative costs for Europe’s organic chemical sector, leading to higher product prices. This trend is confirmed by comparing the price index of basic organic chemicals in intra-EU trade with the corresponding index for Chinese exports. The following chart illustrates the price dynamics between the two.

Price indices for basic organic chemicals in the EU and China

The two indices moved in near-perfect alignment until 2021. After that point, Chinese prices rose less than EU prices during upswings and fell more sharply during downturns. The cumulative effect over three years is significant: between 2021 and 2024, EU prices increased by 3%, while Chinese prices fell by 20%. This implies that, all else being equal, Chinese basic chemical products have gained a cost advantage of over 20% in the past three years.

Do you want to stay up-to-date on commodity market trends?

Sign up for PricePedia newsletter: it's free!

Implications for European Chemical Buyers

The significant price advantage accumulated by Chinese chemical products compared to their EU-traded counterparts makes it essential for chemical buyers to carry out a comparative analysis. This should assess both the technical characteristics and pricing of products traded within the EU versus those exported from China, to determine whether potential cost savings are offset by lower technical quality or reduced guarantees offered by Chinese suppliers.

Of course, before making any decision, buyers must also evaluate the additional risks associated with imports from China, including geopolitical risks, counterparty risks, and logistical challenges.

While the assessment is undoubtedly complex, any sourcing strategy for basic organic chemicals must now take into account the China option, given its current and potential competitive advantages.

Conclusions

In the first quarter of this century, China’s chemical industry has experienced extraordinary growth. Whereas at the beginning of the century, only a handful of chemical compounds were being exported from China, by 2024 the country not only offers a wide variety of chemical exports but, in many cases, holds dominant positions in global trade.

Following its success in inorganic chemistry, China has recently made significant strides in organic chemistry as well. No European chemical buyer can afford to overlook the China option when defining their sourcing strategy.

You may be interested in:

From raw materials to markets: how prices are formed in basic petrochemicals

Published by Luigi Bidoia. .

Organic Chemicals Petrolchimica Price DriversNafta, gas naturale e catrame: tre percorsi che convergono nei grandi mercati degli idrocarburi alcheni e aromatici [ Read all ]

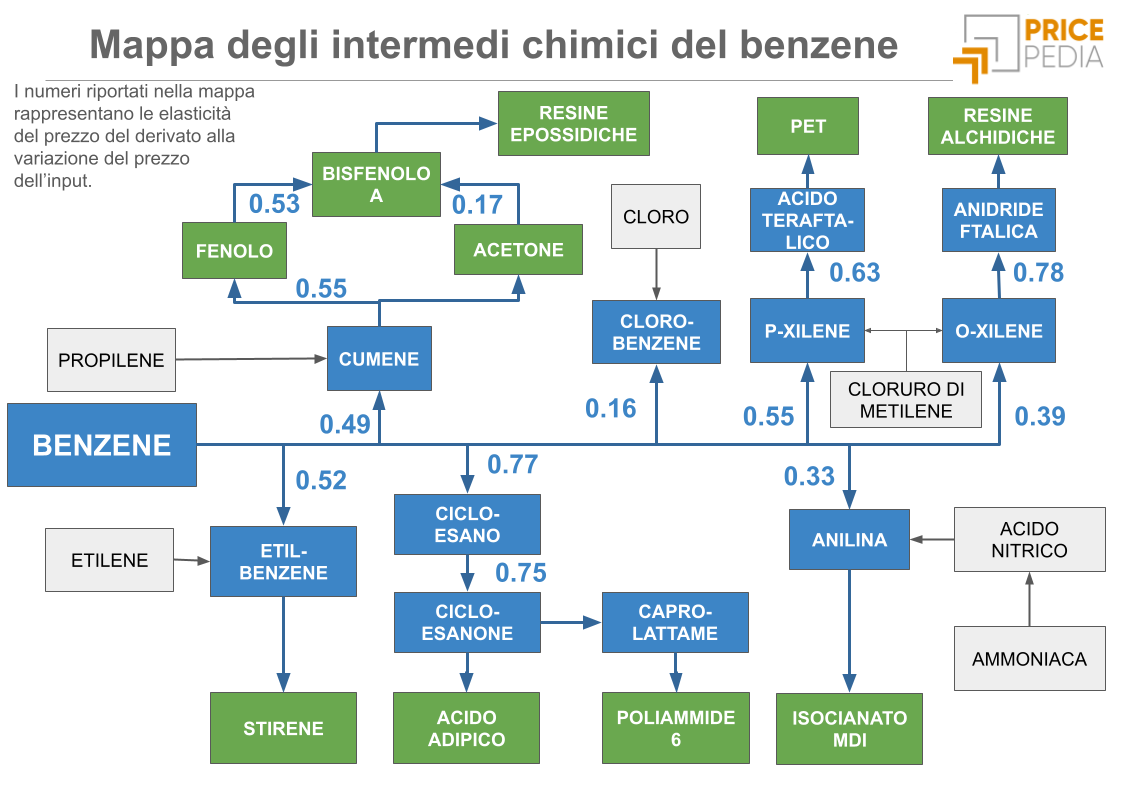

Benzene: A Global Price for a Strategic Supply Chain

Published by Luigi Bidoia. .

Organic Chemicals Cost pass-throughDalla formazione del benchmark mondiale alle ricadute sui costi e sui prezzi dei derivati chimici [ Read all ]

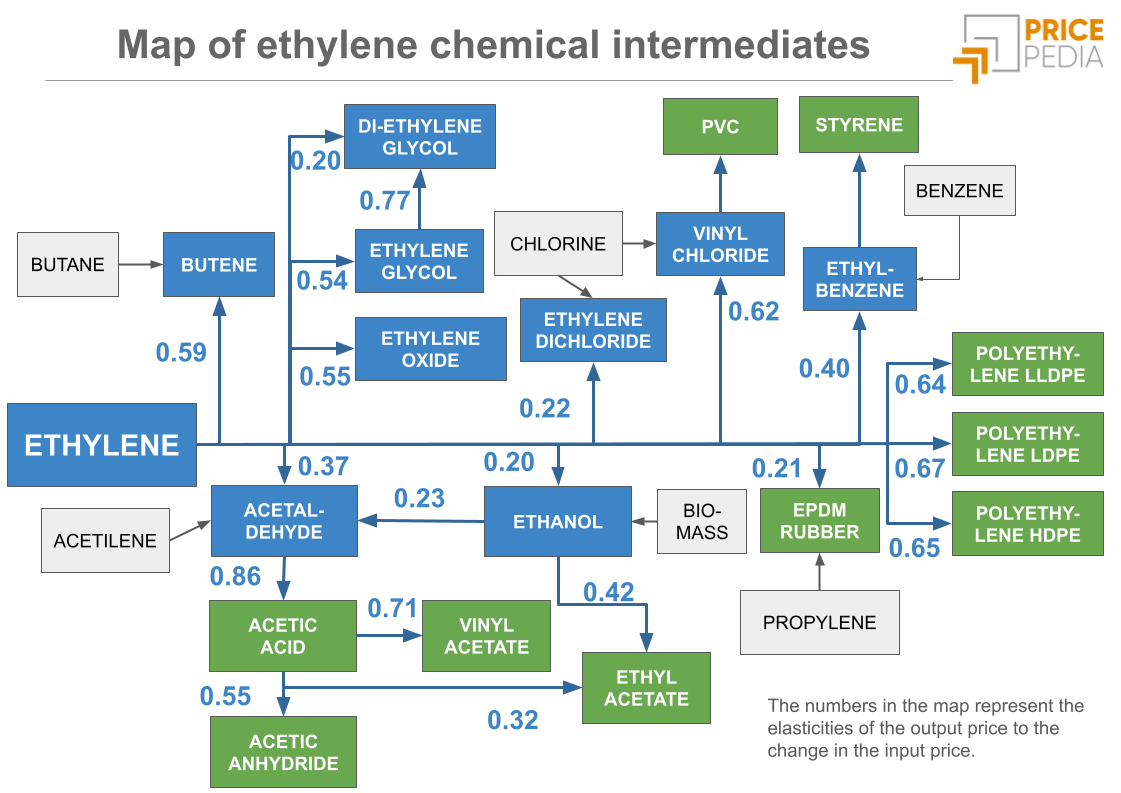

Ethylene: Price Dynamics and Competitive Advantage Between the US and Europe

Published by Luigi Bidoia. .

Organic Chemicals Cost pass-throughCome le variazioni del prezzo dell'etilene si trasferiscono sui prezzi dei derivati [ Read all ]